AGRICULTURAL PARTNERSHIPS BETWEEN SOUTH AFRICA AND SOUTHEAST ASIA UNDER BRICS+

By: Buhlebemvelo Dube and Matume Maila

Introduction

The evolving landscape of international trade, as seen by the increasing prominence of the BRICS economic alliance, which includes Brazil, Russia, India, China, and South Africa, presents an important background for reviewing agricultural trade dynamics between Southeast Asia and South Africa. These dynamics are characterized by a complex interplay of factors, including the potential for enhanced trade flows and diversification of agricultural markets, alongside inherent challenges stemming from regulatory environments, infrastructural deficits, and the pervasive influence of global market volatility. This analysis examined agricultural trade relations between Southeast Asia and South Africa, revealing both possible opportunities and constraints in an emerging BRICS context.

Discussion

The expansion of BRICS+ is set to impact the Association of South-East Asian Nations (ASEAN) on account of Indonesia joining BRICS+. The positioning of Indonesia as a launchpad for accelerated trade is set to have an economic impact on both ASEAN and BRICS+ since it is a key member of ASEAN and is the largest economy in the Southeast Asia. ASEAN group is comprised of Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam (Council on foreign relations, 2025). Table 1 below depicts the top ten traded agricultural products by South Africa and ASEAN. The agricultural trade balance between ASEAN and South Africa is worth roughly $1.56 billion. The two partners trade significant commodities such as rice, palm oil, vegetable fats, palm kernel, and cocoa butter. South African exports to the ASEAN grouping are valued at around $5.25 billion, and there is still room to improve market access through the BRICS+ expansion to open new prospects. Raw cane sugar, fresh apples, fresh or dried oranges, fresh grapes, fresh pears and soya beans are respectively the dominant agricultural commodities South Africa exports to ASEAN.

Table 1: Major agricultural trade commodities between South Africa and ASEAN

| SA’s top 10 exports | SA’s top 10 imports | |||

| Commodity | Export value ($) 000 | commodity | Import value ($) 000 | |

| 1 | Raw cane sugar | 122 103 | rice | 469,929 |

| 2 | Fresh apples | 85 743 | Palm oil | 428,998 |

| 3 | Fresh or dried oranges | 52 442 | Vegetable fats | 69,777 |

| 4 | Fresh grapes | 35 456 | Palm kernel | 32,842 |

| 5 | Fresh pears | 30 829 | Cocoa butter | 27,478 |

| 6 | Soya beans | 25 451 | Cocoa powder | 18,979 |

| 7 | Fresh cranberries, bilberries and other fruits of the genus Vaccinium | 15 675 | Pepper | 10,583 |

| 8 | Fresh or dried mandarins incl. tangerines and satsumas (excl. clementines) | 15 496 | Broken rice | 8,900 |

| 9 | Cotton | 15 123 | Pasta | 8,083 |

| 10 | Fresh or dried macadamia nuts, shelled | 12 741 | Fresh or dried cashew nuts | 7,817 |

Source: ITC (2025)

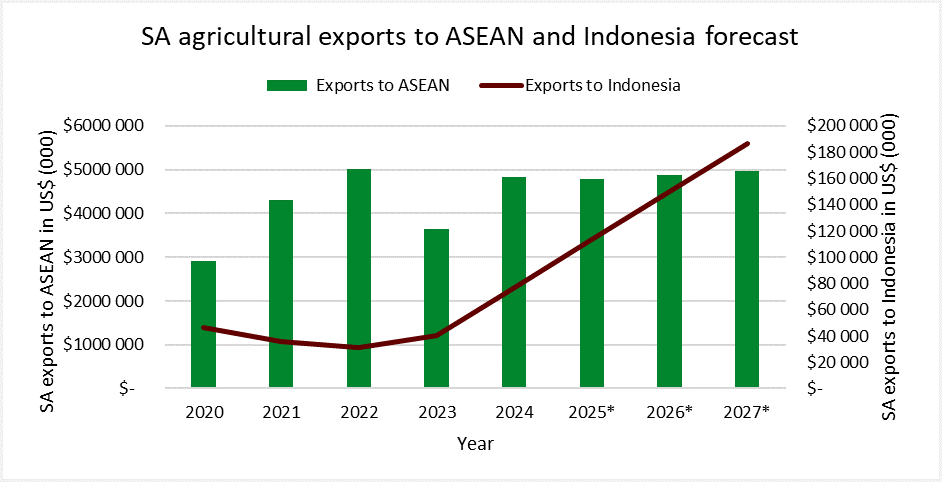

Figure 1 below depicts a steady recovery or stabilization in trade performance of almost $36 million between 2023 and 2024, which is underpinned by improved logistics, or regional trade cooperation (e.g., BRICS+) which boosts market confidence. This is appropriate considering the potential growth of market access under the BRICS+ partnership. Furthermore, ASEAN, is forecast to experience considerably lower increases than Indonesia. This is reasonable given the strong trade relations between South Africa and Indonesia, compared with some ASEAN countries, and that it is much effortless to negotiate with a single nation than a block. Key agricultural commodities earmarked for the Indonesian and ASEAN group include fresh apples, fresh grapes, sugar cane, and oranges.

Figure 1 also predicts agricultural trade trends between Southeast Asia and South Africa, with a focus on Indonesia from 2020 to 2027. It can be observed that the agricultural exports from South Africa to Indonesia are likely to expand progressively over the next three years. The three-year forecast shows that the export will increase by almost $72.9 million between 2025 and 2027. The model predicts stable growth following the volatility witnessed between 2020 and 2024.

Figure 1: SA agricultural exports and Indonesia forecast

Source: ITC (2025) & NAMC calculations (2025)

Indonesia is a key market for South African fruits and sugar cane. The two partners have strong trade relationships and there is significant potential for further market access. The BRICS+ expansion will enable South Africa to develop enhanced trade facilitation frameworks with ASEAN group. This is important towards reducing the high tariff and non-tariff barriers between these partners. Furthermore, there are opportunities for Africa and ASEAN to intensify regional dialogues, with Africa already underway with its African Continental Free Trade Area (AfCFTA) agreement. These opportunities can ensure that South Africa expands market access and diversifies its export basket which is critical for sustainable growth in exports.

Conclusion

Given the varied agricultural capabilities of each region, there is clear potential for enhanced trade complementarity between Southeast Asia and South Africa. Furthermore, interest by both Malaysia and Thailand to become members of BRICS would further open market access to the Southeast Asian region for South African exporters.

INSIGHTS