CAN BRICS DRIVE EXPORT GROWTH IN SOUTH AFRICAN AGRICULTURE?

By: Buhlebemvelo Dube, Solly Molepo and Victor Thindisa

The strategic location of the Republic of South Africa, in terms of the prominent Cape Sea Route shipping transit corridor, provides a preferred route for vessels bypassing the Suez Canal. The Republic’s membership in organisations such as BRICS+ positions the country as an important player in international trade and regional integration. The international trade environment is increasingly becoming more complex, unpredictable, and volatile. This is problematic for developing nations, such as South Africa, which exports 70% of its total agricultural production. Agricultural exports destined to BRIC countries are valued at $1.1 billion, Africa ($5.9 billion), Europe ($3.9 billion), Asia ($2.8 billion), and the Americas at $827 million. A rise in trade disruptions exposes South Africa’s exports to considerable uncertainty in its quest for market access. Whilst these challenges expose the Republic to export disruption, it’s also an opportunity for South Africa to diversify its export base. South Africa is a member of the BRICS+ countries. An analysis of how the country can unlock trade opportunities within the bloc and thus safeguard market access is necessary. Market access erosion, driven by rising tariffs, non-tariff barriers, and geopolitical realignments, poses a threat to the livelihoods of rural communities and the viability of agribusinesses across the entire value chain. Against this backdrop, the expansion of BRICS into BRICS+, coupled with commitments made in the 2025 Rio Declaration, offers a timely window for South Africa to secure new preferential market access, especially in Asia, Latin America, and West Africa. South Africa needs to initiate trade agreements and protocols with its BRICS+ partners to unlock export opportunities.

South Africa’s tariff regime is characterised by a domestically liberalised structure with considerable outward exposure. The Most Favoured Nation (MFN) applied tariff averages 7.6% across all goods, while agricultural products face a higher average of 11.4%, positioning the country among moderately open economies for agricultural imports. Notably, only 41.5% of agricultural tariff lines are bound, compared to full coverage (100%) in most BRICS+ peers, constraining South Africa’s flexibility to introduce new protective measures. At the same time, 37.8% of all tariff lines are duty-free, underscoring the relatively open nature of the tariff framework. The highest tariff peaks are concentrated in sensitive agricultural subsectors such as dairy products (up to 96%) and meat and edible offal (up to 82%), which reflects strong defensive interests in these industries. Recent data from the World Trade Organisation reports reveal a wide divergence in MFN applied tariffs across BRICS+ members. Notably, India and Nigeria impose high average agricultural tariffs (India: 50.8%; Nigeria: 120.5%), yet also show increasing import volumes in horticultural, cereal, and livestock products, which signals demand-driven access opportunities. China and Vietnam show lower simple agricultural averages (China: at 10.0%, Vietnam: 7.6%) with broader duty-free treatment in select subsectors, including citrus, nuts, and processed foods. Russia and Brazil, though net exporters, offer complementary seasonal access windows where counter-cyclical trade can be advantageous (e.g., off-season exports of grapes, pears, avocados). Thus, South Africa’s high-quality, counter-seasonal produce, SPS compliance, and preferential SADC logistics corridors position it well to supply high-value commodities into these expanding markets.

The country’s key import partners include Brazil, India, Argentina, and increasingly Russia and China, driven by fertilizers, cereals, and animal feed additives. These are strategic partners within BRICS+ countries. Top export products include citrus, wine, grapes, nuts (macadamia, almonds), wool, and sugar, with a growing presence in avocados and blueberries. Some of the top exported products have gained market access in key markets, and this growth boosts optimism for the future. Nevertheless, the dual vulnerability remains in the form of high reliance on commodity exports with price elasticity, and increased dependence on a narrow pool of partners, mostly outside Africa. These weaknesses make it not only economically sound to diversify exports to BRICS+, but it’s strategic as a means to keep abreast of rising protectionism. Lack of tangible trade arrangements within BRICS has been a significant hurdle. Despite this, agricultural exports, between 2020 and 2024, rose by $194 million, totalling an estimated $1.1 billion in 2024. However, growth remains underwhelming, largely due to the following: (i) absence of a dedicated BRICS+ trade agreement; (ii) divergent and complex applied MFN tariffs and Non-Tariff Barriers (NTB), as well as (iii) complex Sanitary and Phytosanitary (SPS) protocols.

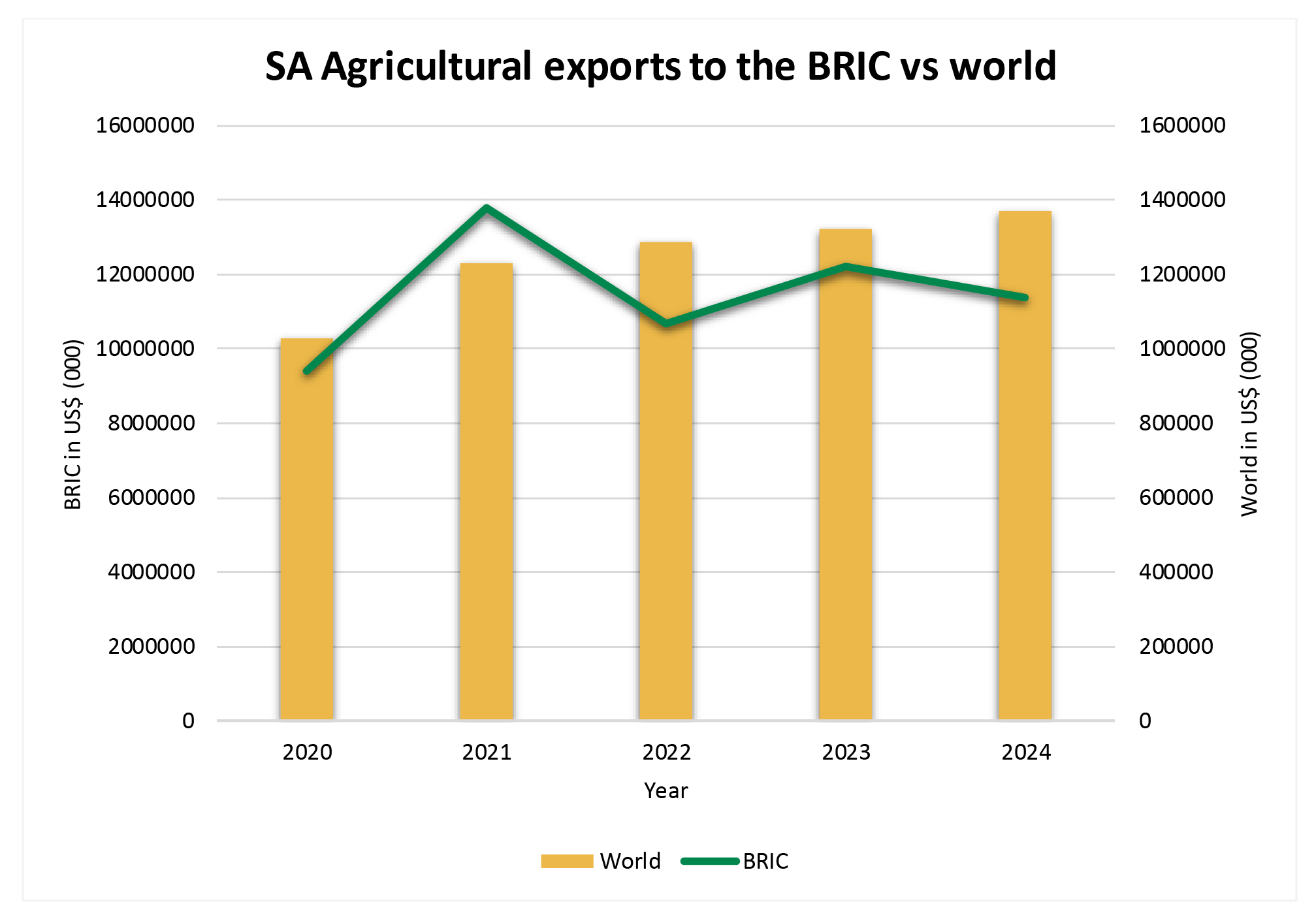

Recent trade figures from the International Trade Centre (ITC), as depicted by Figure 1 below, underscore the untapped potential of agricultural exports into BRIC markets, particularly China and India. Despite agricultural exports’ value to BRIC reaching $1.1 billion in 2024, this accounted for less than 10% of its global agricultural exports, which stood at $13.7 billion in the same year. Products such as macadamia nuts in shell ($125 million), fresh oranges ($108 million), and greasy shorn wool ($198 million) represented leading export lines into BRIC, yet their volumes remained modest relative to BRIC’s aggregate import demand. For instance, BRIC nations collectively imported over $1.1 billion worth of fresh apples and $597 million in mandarins globally in 2024, while South Africa’s BRIC-bound exports of these products amounted to just $70 million and $95 million, respectively, highlighting a significant supply gap that South African producers are well-positioned to fill.

Figure 1: South African agricultural exports to the world and the BRIC countries between 2020 and 2024

Source: Author`s calculations based on ITC calculations from the South African revenue services (2025

Similarly, high-value commodities such as fresh grapes and pears, where South Africa holds a competitive and counter-seasonal advantage, remain underrepresented in BRIC markets. This persistent trade asymmetry is underpinned by a critical misalignment between South Africa’s export portfolio and BRIC+ consumption trends, reinforcing the need for calibrated, product-specific interventions. These include targeted SPS protocol negotiations, logistics upgrades, and trade promotion strategies under the BRICS Agriculture Cooperation Mechanism. These data-driven insights support the broader strategic imperative that South Africa must transcend generic BRICS diplomacy and embark on deliberate, commercially grounded trade offensives to fully harness the export potential of BRICS+. Further analysis reveals an even deeper trade gap. While we exported approximately $1.1 billion in agricultural goods to BRIC in 2024, BRIC’s combined agricultural import bill surpassed $272 billion, placing our market penetration rate at a mere 0.04%. This stark figure illustrates the extent of marginalization faced by South Africa within a bloc where it holds political membership but wields limited commercial leverage. The 2025 BRICS Rio Declaration offers a policy-aligned remedy by reaffirming core WTO principles, including Special and Differential Treatment (S&DT) and NTB reduction. These provisions directly respond to structural hurdles impeding South African exports, such as SPS misalignment and regulatory opacity.

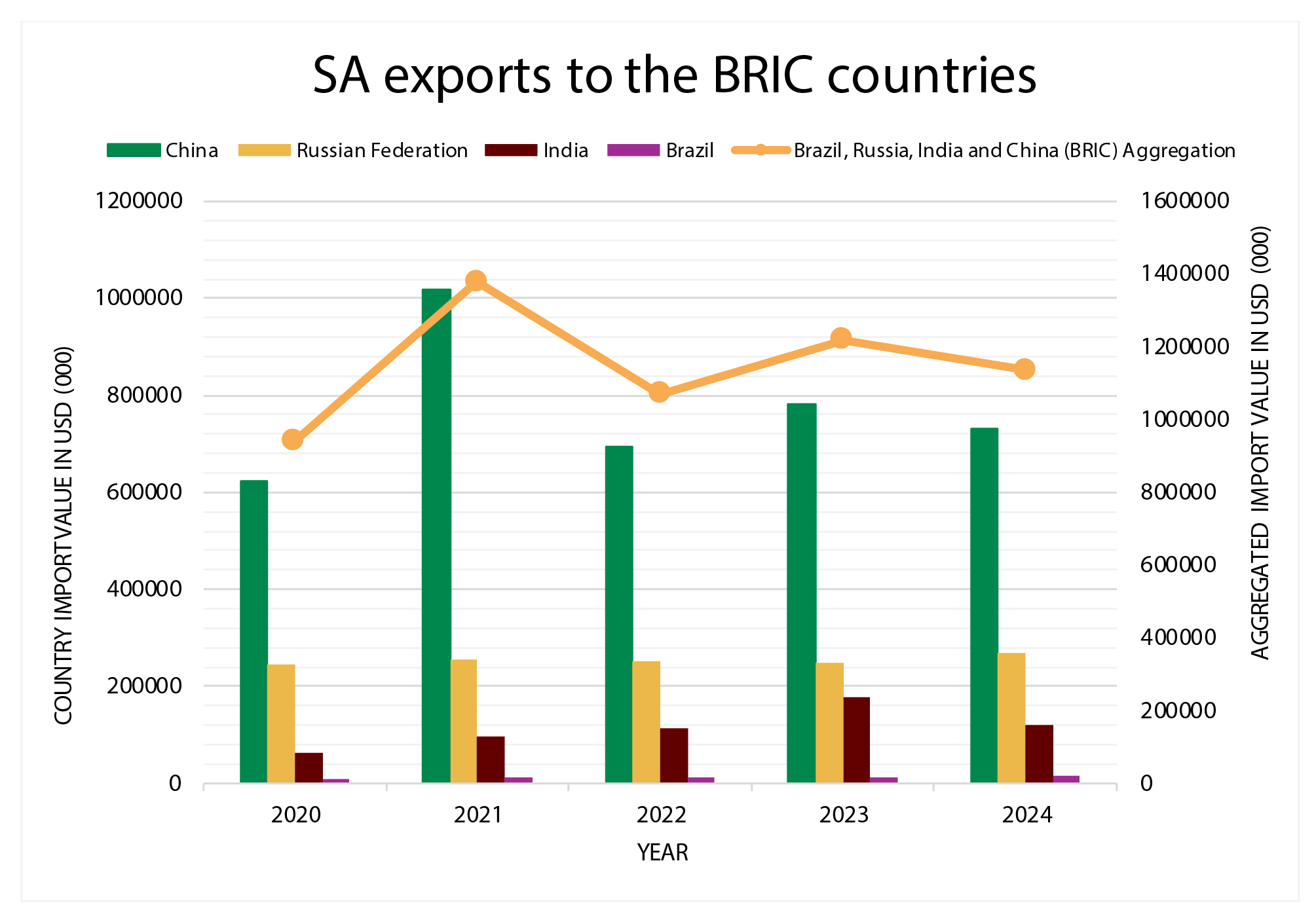

Figure 2 below shows exports into the BRIC countries. China has been a dominant and important trade partner of South Africa within BRICS, with a 70% share in the total portion of exports. The Chinese market`s potential cannot be ignored, especially with the recent trade developments, which seek to further open up the market for African countries as a whole. South Africa’s trade complementarity with China and India is robust, driven by their demand for primary commodities, a category under which raw and semi-processed agricultural exports fall. Post 2010, South Africa’s export surplus to BRICS has widened, surpassing that to the European Union (EU) in key years, underlining trade creation rather than diversion. However, intra-BRICS trade is skewed toward low-processed commodities, limiting value-added agricultural exports. This underscores the need for targeted interventions to restructure export portfolios, aligning with BRICS+ consumption trends such as ready-to-eat foods, dairy, plant-based proteins, and specialty crops (e.g., rooibos, macadamia, essential oils). Therefore, it becomes crucial to question whether the declaration has any impact on the potential to expand market access. The 2025 Rio Declaration provides an enabling policy environment which took a stance that reaffirms the rules-based multilateral trading system, which would enhance predictability for exporters.

Figure 2: SA agricultural exports to the BRIC countries between 2020 and 2024

Source: Author`s calculations based on ITC calculations from the South African revenue services (2025)

India’s import demand for fresh apples in 2024, juxtaposed with South Africa’s modest $70 million in total BRIC-bound apple exports, strongly suggests the presence of unresolved NTBs, precisely the kind of friction the Declaration’s harmonisation agenda aims to address. Comparable patterns persist across product categories. South Africa’s global orange exports totalled $758 million, yet only $107 million entered BRIC markets. Mandarins earned $581 million globally, but under $96 million from BRIC. These trade bottlenecks present a compelling case for activating the Declaration’s calls for agro-logistics enhancement, regional SPS alignment, and food security cooperation. By addressing these structural gaps, South Africa could strategically reposition its citrus, nut, grape, and wool exports into higher value segments across BRICS+ urban markets, many of which are shifting toward premium, health-conscious, and climate-resilient food products. Thus, a strong argument can be made to suggest that there is progress in creating a conducive trade environment for the bloc`s members, especially for South Africa.

South Africa’s ability to unlock BRICS+ opportunities rests on aligning trade concessions with SPS reforms and agricultural logistics and investment to drive sustainable export growth. The BRICS+ expansion marks a tectonic shift in global trade architecture with an opening that could decisively reposition South Africa’s agriculture sector. The 2025 Rio Declaration provides the institutional and policy scaffolding to address long-standing constraints such as tariff unpredictability, NTBs, SPS misalignment, and climate protectionism. Through product-specific trade-offensives, logistics reform, and harmonised standards, South Africa can unlock differentiated access into high-value BRICS+ markets. Yet this opportunity is not automatic. Without assertive, evidence-led diplomacy and agro-industrial upgrading, South Africa risks remaining a politically included yet commercially excluded partner. The challenge now is not whether BRICS+ could unlock growth, but whether South Africa will act boldly enough to claim it.

Below is the full TRADE RESEARCH COMMENTARY.