SOUTH AFRICA’S WHEAT INDUSTRY UNDER REVIEW: UNDERSTANDING THE SECTION-7 COMMITTEE INVESTIGATION

By: Thandeka Ntshangase, Buhlebemvelo Dube, and Mahlogedi Thindisa

Pursuant to the request by the wheat industry to the Minister of Agriculture and the National Agricultural Marketing Council (NAMC), the Section-7 Committee (“the Committee”) as per the Marketing of Agricultural Products Act (Act No. 47 of 1996, as amended) was established to investigate the structural and policy constraints that affect the competitiveness of the domestic wheat industry (Plaas, 2025). The Committee is mandated to examine trade policy, institutional, regulatory, and value chain challenges that confront the wheat industry and provide evidence-based recommendations to the Minister’s for consideration. The investigation reflects growing concern that the industry’s challenges extend beyond seasonal production conditions and require a comprehensive assessment of the trade policy, structure, and operating environment (Day & Vink, 2019; Meyer & Kirsten, 2005). As a strategic staple commodity, wheat plays a central role in South Africa’s food system. The competitiveness and resilience of the domestic wheat value chain is an important priority for the sector and household food security (Dube et al., 2026).

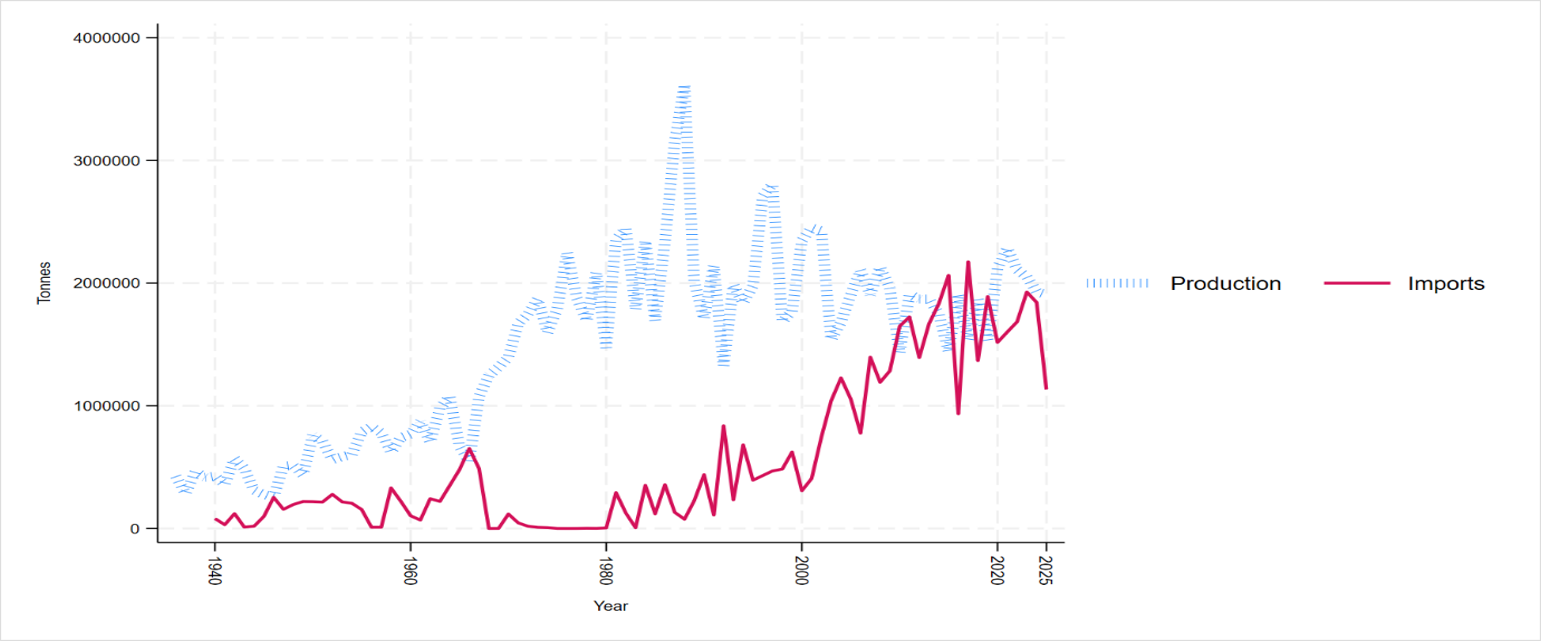

The challenges confronting the wheat industry should be appreciated from multiple perspectives viz: (i) the global market dynamics, (ii) industry competitiveness and growth, and (iii) domestic food security. The latest estimates from the Crop Estimates Committee (CEC) indicate that South Africa produced 1.91 million tonnes of commercial wheat from 517 300 hectares in the 2025 production season (CEC, 2026). Although the final crop exceeded the February estimate by 0.44%, wheat remains the country’s largest winter cereal, underscoring its strategic importance to national food security and the broader grain economy. Figure 1 below depicts that domestic wheat production has increased substantially over the past nine decades (Dube et al., 2026; Erenstein et al., 2022). However, production growth has been characterised by considerable interannual variability and has not eliminated the need for imports. Since the early 2000s, wheat imports have risen markedly, indicating that domestic supply has increasingly relied on international markets to meet national requirements.

Figure 1: South Africa’s wheat production and imports (1936–2025)

Source: NAMC calculations based on Wheat Board (1954, 1971, 1995, 2012 and 2014 Statistical Abstracts); Wheat Board Basic Statistics (June 1997); South African Grain Information Service (SAGIS), 1997/98–2024/25.

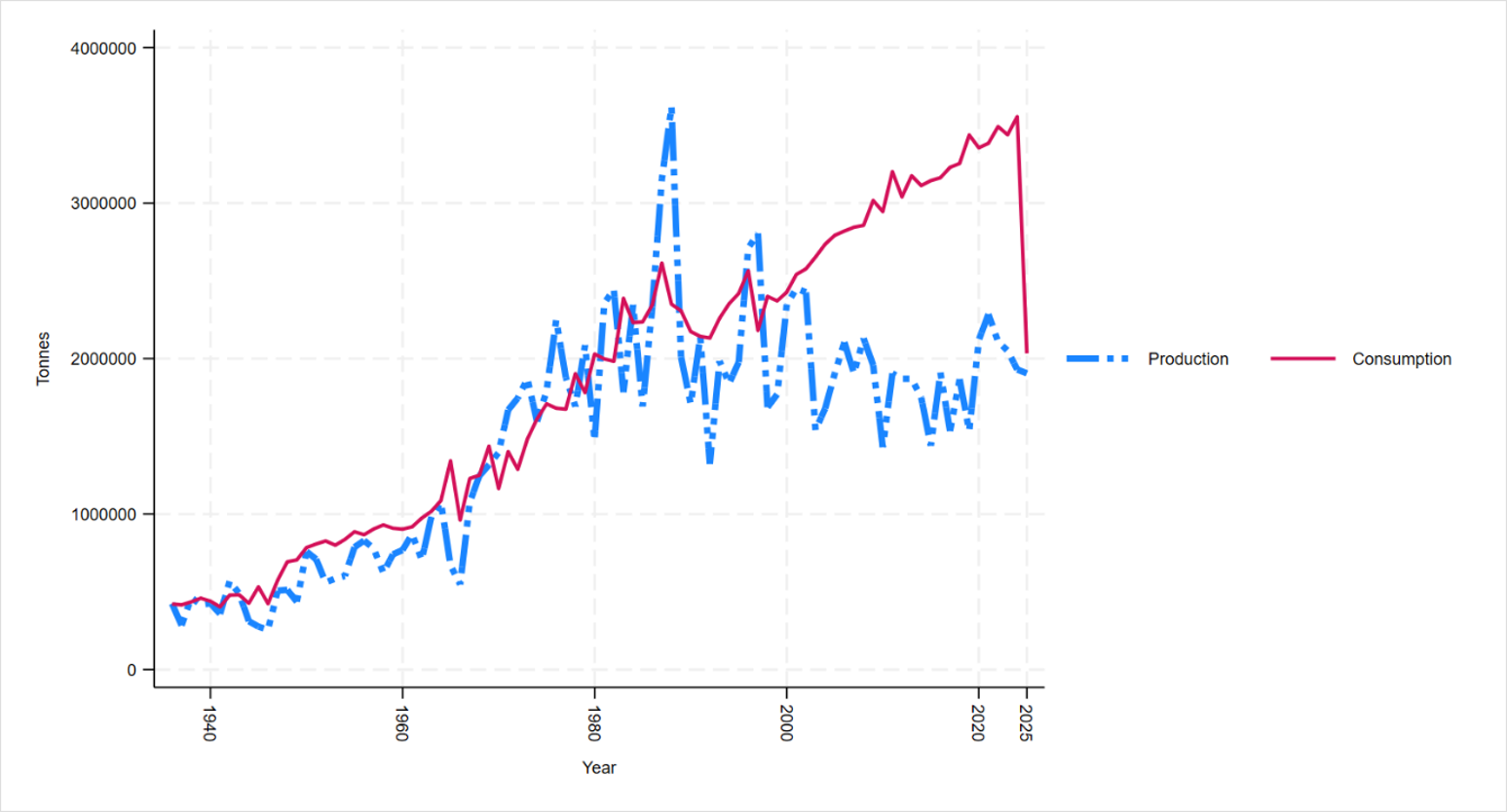

The structural imbalance is reinforced in Figure 2 below, that compares domestic wheat production with domestic consumption. While wheat consumption has followed a relatively steady upward trajectory, production has fluctuated around a comparatively stable level. The widening gap between production and domestic utilisation demonstrates that demand has consistently outpaced domestic supply, requiring imports to bridge the deficit.

Figure 2: South Africa’s wheat consumption and production

Source: NAMC calculations based on Wheat Board (1954, 1971, 1995, 2012 and 2014 Statistical Abstracts); Wheat Board Basic Statistics (June 1997); South African Grain Information Service (SAGIS), 1997/98–2024/25

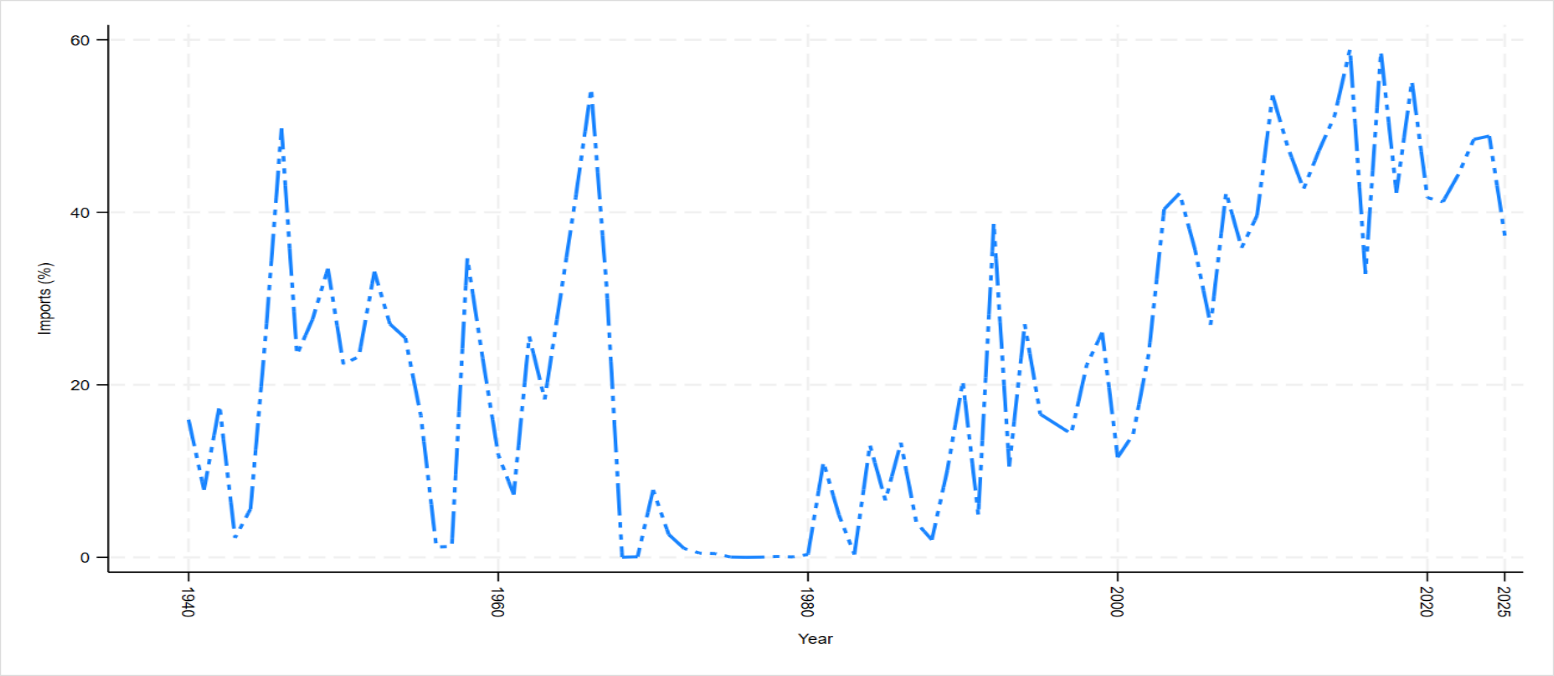

Consequently, Figure 3 below depicts that South Africa’s import dependency has increased over time. Whereas imports historically represented a relatively small share of total wheat availability, over the last couple of decades, imports account for a substantial proportion of domestic supply (Bester, 2014; Liebenberg & De Wet, 2018).This growing reliance on imported wheat exposes the industry to external shocks such as (i) international price volatility, (ii) exchange-rate movements and (iii) global supply disruptions, (iv) climate variability, and (v) erosion of multilateral trade system. These shocks reinforce the rationale for a comprehensive review of the structural, policy and institutional factors affecting the competitiveness of the domestic wheat industry.

Figure 3: Import dependency in the South African wheat market, 1936/37–2024/25

Source: NAMC calculations based on Wheat Board (1954, 1971, 1995, 2012 and 2014 Statistical Abstracts); Wheat Board Basic Statistics (June 1997); South African Grain Information Service (SAGIS), 1997/98–2024/25

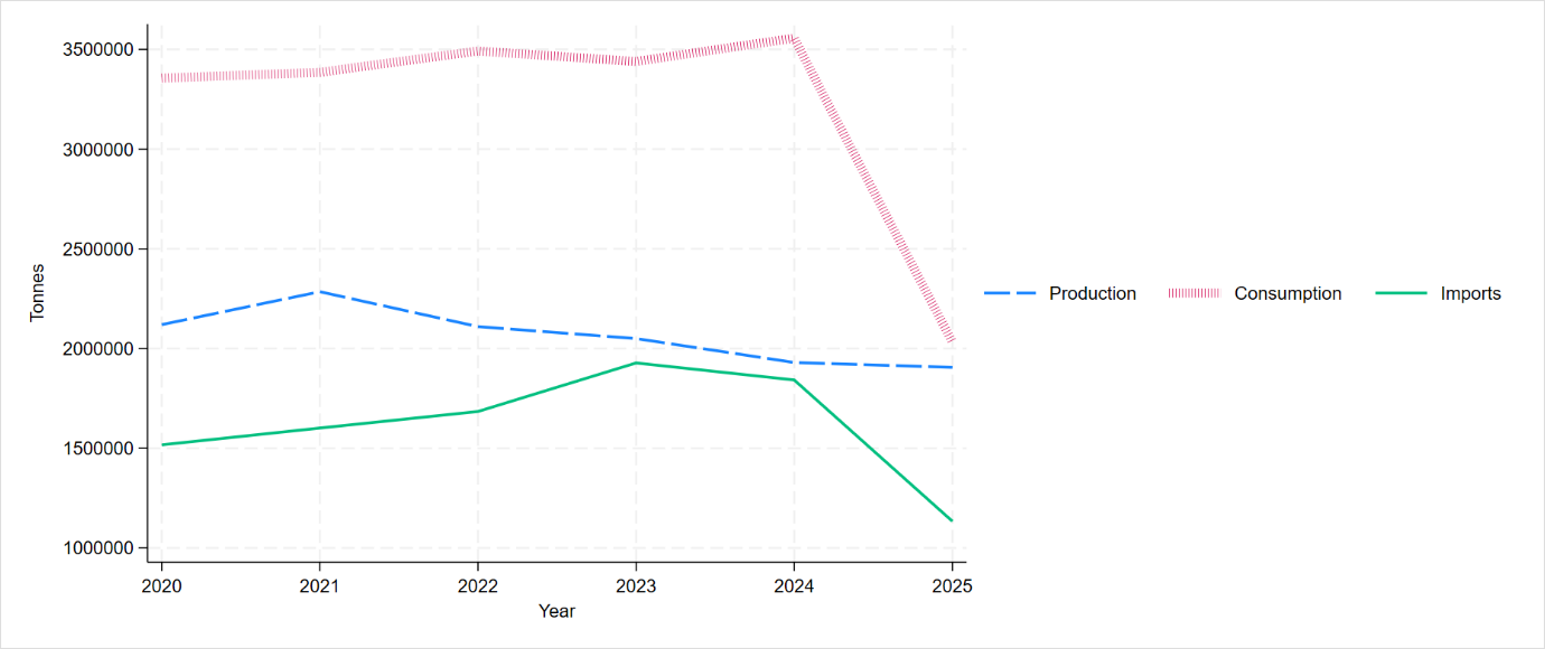

Figure 4 below depicts that domestic wheat production remained below consumption between 2020 and 2025, requiring imports to bridge the supply gap. Although annual production fluctuated, imports continued to play a critical role in meeting domestic demand. The final calculated commercial wheat crop of 1.91 million tonnes for the 2025 production season reinforces the structural nature of South Africa’s reliance on imported wheat and the continuing relevance of the Section 7 investigation.

Figure 4: Recent developments in South Africa’s wheat market, 2020–2025

Source: NAMC calculations based on South African Grain Information Service (SAGIS)

The long-term trends in production, consumption and trade confirm that the challenges facing South Africa’s wheat industry are structural and unresponsive trade policy that warrant a comprehensive assessment of the policy, institutional and market environment (Dube et al., 2026; Silva et al., 2023). Accordingly, the Section-7 Committee is mandated to examine the structural, trade policy, institutional and regulatory factors affecting industry competitiveness across the wheat value chain and to develop evidence-based recommendations for the Minister of Agriculture.

Since its establishment in May 2026, the Committee has adopted its Terms of Reference, refined its analytical scope, broadened stakeholder participation, established thematic workstreams and commenced with technical assessments. Consistent with the social compact approach by the Agriculture and Agro-processing Master Plan (AAMP), the Committee adopted the workstream approach as an appropriate methodology for conducting the investigations. Workstreams are constituted by various value chain actors. Workstream is defined as parallel track of activities, tasks, and deliverables focused on specific objective and theme. The workstream disaggregates large, complex themes into manageable segments, allowing different groups to contribute simultaneously whilst contributing to the overall objective of the investigation.

The various workstreams focuses on the following functional themes: (i) tariff dispensation and trade policy on wheat and wheaten products, (ii) value chain, storage, infrastructure, and logistics constraints, (iii) transformation and inclusivity along the value chain, (iv) food security, biosafety, innovation, and new breeding techniques.

The next phase of activities by the Committee would focus on stakeholder submissions, technical analysis and evidence gathering, culminating in recommendations to strengthen the competitiveness, resilience and long-term sustainability of South Africa’s wheat industry.

REFERENCES

Bester, M., 2014. Dominant factors which influence wheat production in South Africa. Stellenbosch: Stellenbosch University.

Crop Estimates Committee (CEC), 2026. The final area planted and crop production figures of winter cereals for the 2025 production season. Pretoria: Department of Agriculture.

Day, M. & Vink, N., 2019. The distortions to incentives in South African agriculture: A case study of the wheat industry. Agrekon, 58(3), pp.292–307.

Dube, B., Mabhunu, N., Lungwana, M., Molepo, S., Kau, J. & Moswane, L., 2026. Structural, climatic, and cost drivers of wheat production in South Africa: An ARDL analysis (1990–2022). Frontiers in Sustainable Food Systems, 10, 1762581.

Erenstein, O., Jaleta, M., Mottaleb, K.A., Sonder, K., Donovan, J. & Braun, H.-J., 2022. Global trends in wheat production, consumption and trade. In: Wheat Improvement: Food Security in a Changing Climate. Cham: Springer International Publishing, pp.47–66.

Liebenberg, I. & De Wet, F., 2018. Food security, wheat production and policy in South Africa: Reflections on food sustainability and challenges for a market economy. TD: The Journal for Transdisciplinary Research in Southern Africa, 14(1), pp.1–11.

Meyer, F. & Kirsten, J., 2005. Modelling the wheat sector in South Africa. Agrekon, 44(2), pp.225–237.

Plaas, 2025. Wheat farmers financially strained as Section 7 looms. Available at: https://agriorbit.com/wheat-farmers-financially-strained-as-section-7-investigation-looms/ [Accessed 29 June 2026].

Silva, J.V., Jaleta, M., Tesfaye, K., Abeyo, B., Devkota, M., Frija, A., Habarurema, I., Tembo, B., Bahri, H. & Mosad, A., 2023. Pathways to wheat self-sufficiency in Africa. Global Food Security, 37, 100684.

South African Grain Information Service (SAGIS), 2026. Historic wheat statistics, 1936/37–2024/25. Pretoria: South African Grain Information Service.

South African Grain Information Service (SAGIS), Wheat Board and Crop Estimates Committee (CEC), 2026. Historic Wheat Statistics, 1936/37–2024/25. Statistical compilation of wheat production, consumption, imports and producer deliveries. Updated 26 May

POLICY BRIEF